.svg)

There are numerous car finance agreement structures out there, so being informed on the most common types is important when exploring your car finance options. Ayan offers a Shariah compliant version of HP, called Ijara wa Iqtina, yet currently we do not have a Shariah compliant version of PCP (or have looked into whether this is even possible).

This article touches only on the general structure of both, to help you understand and decide which would work best for you, no matter where you decide to get your car financed.

What Is HP (Hire Purchase)?

Hire Purchase (HP) is a car finance option where you make monthly payments towards owning the car outright. It starts with a deposit, usually around 10%, followed by a series of fixed payments over 3 to 5 years. Once the final payment is made, the car is fully yours, no extra fees or final lump sums to worry about.

There are no mileage limits, and since there's no large balloon payment at the end, it’s a straightforward way to own a car. If you’re someone who plans to keep the car long-term and prefers clear, predictable costs each month, HP is a good fit. It’s simple, easy to understand, and gives you full ownership at the end of the term.

What Is PCP (Personal Contract Purchase)?

PCP is a more flexible, but slightly more complex, car finance option. Unlike Hire Purchase, you’re not paying off the full cost of the car, you’re covering the depreciation during the contract term. That’s why monthly payments tend to be lower than HP. You’ll usually put down a deposit of around 10%, followed by monthly payments over 2 to 4 years.

At the end of the agreement, you’ve got three options: hand the car back, trade it in for a new one, or pay a final “balloon payment” to own it. That final payment can be a few thousand pounds, so it's worth planning ahead if ownership is your goal.

Most PCP deals come with mileage limits and vehicle condition requirements. Go over the limit or return the car in poor condition, and you could face extra charges. PCP is a great fit if you like switching cars every few years, want lower monthly costs, and don’t necessarily need to own the car at the end.

Key Differences Between HP and PCP

1. Ownership

HP: Your contract and monthly payments are set up so that the final payment on your schedule, is your last payment. After that, you will automatically own the car - this is normally written into the original agreement. However, make sure you read your agreement before signing, some companies might charge you another extra fee on top to transfer ownership.

PCP: You only own the car if you choose to make the balloon payment at the end. You also have the option to return the car, or some companies might let you upgrade to a newer car at a discounted rate.

2. Monthly Payments

HP: Higher monthly payments because the goal is to pay off the entire car by the end of the contract.

PCP: Lower monthly payments because you're only paying for the depreciation that has been incurring, rather than trying to pay off the car, leaving the balloon payment option at the end which would cover the entire cost of the car (accounting for the depreciation costs you have already paid).

3. Final Payment

HP: No large payment at the end, just regular monthly instalments. But as mentioned earlier, some finance agreements might include a mandatory 'fee' to transfer ownership. Always make sure you read your finance agreement carefully and check with the finance company should you have any doubts.

PCP: Optional “balloon” payment to take ownership (can be £5,000+).

.png)

4. Mileage Limits

HP: Generally, no mileage restrictions. But again, this could depend on the finance company.

PCP: Strict mileage limits, exceeding them will likely result in extra charges, as this directly correlates to depreciation of the vehicle.

5. Flexibility

HP: Arguably, less flexible. You make a commitment to owning the vehicle at the end of the contract. You can choose to voluntarily terminate the contract, but you have to have covered at least 50% of the total cost of financing. If you haven't, you'll be asked to cover at least that amount, plus fair wear and tear charges, and possibly some mileage payments. If you have covered 50% already, you'll just be expetected to cover any fair wear and tear costs, plus any costs incurred from going above expected mileage.

PCP: Quite flexible. You can return, trade, or buy the car.

6. Early Settlement / Termination

HP: Settling early is relatively easier, with a lump sum payment that covers the remaining vehicle balance, however, a settlement fee might apply - of course, this means you get to keep the car. However, if you choose to give back the car, and voluntarily terminate, the aformentioned guidelines apply, whereby you will likely be asked to cover 50% of the total financing amount, fair wear and tear costs, and any exceeded mileage.

PCP: More complex; involves calculating the remaining balance and final value. You can always discuss with your financing company to get a better understanding of how they calculate this before you sign the agreement. Stuff happens.

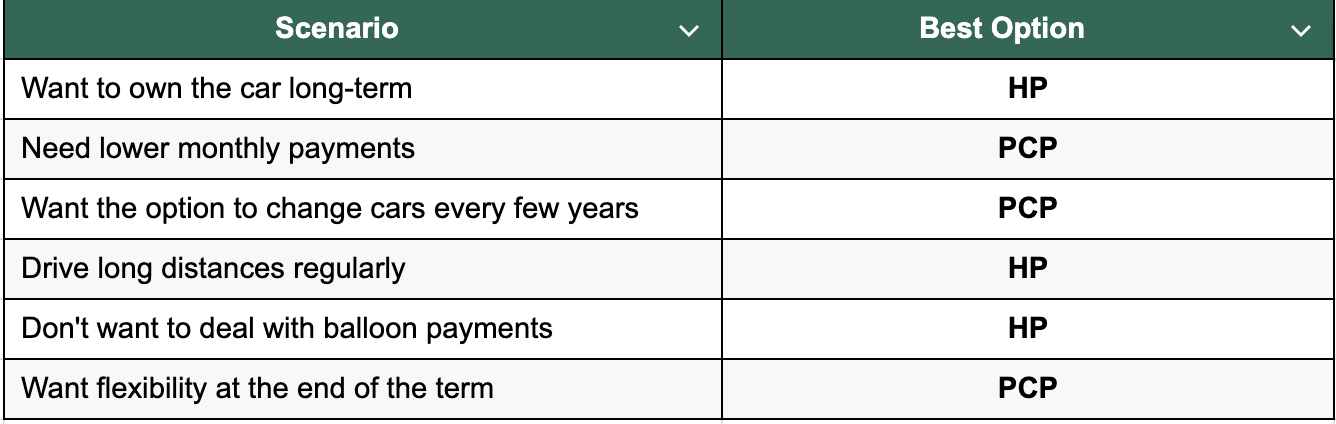

Which One Is Better for You?

Common FAQs

What if I damage the car during PCP?

You may incur charges when returning the car if damage exceeds “fair wear and tear” guidelines.

Can I end my HP or PCP early?

Yes, but with different processes. With HP, you can often settle early. With PCP, early termination may depend on whether you’ve repaid 50% of the total agreement.

Can I modify the car during a PCP or HP agreement?

It depends on the finance provider. With PCP, since you don't technically own the car until the final payment is made, modifications are usually not allowed, especially cosmetic or mechanical changes that affect resale value. With HP, modifications may be possible once a significant portion of the loan is paid off, but you must get written permission from the finance company first.

Always check your agreement terms before making any changes to the vehicle.

Conclusion

Both HP and PCP have their benefits, and choosing the right one depends on your goals.If you want ownership, long-term value, and no mileage limits, go for HP.If you want low monthly costs, new cars every few years, and flexible options, PCP might suit you better.Found this helpful? Share this guide with anyone financing a car, or drop us a message if you need help understanding car finance options in the UK.

.png)